-

转载请注明作者和出处: https://zhuanlan.zhihu.com/p/40447996

-

Github代码获取:https://github.com/jiguang123/Credit-Loans-of-Data-Analysis

-

Python版本: Python3.6

-

运行环境: Win10 + Anaconda + jupyter Notebook + Sublime text3

- 采用了Lending Club 信用贷款违约数据是美国网络贷款平台 LendingClub 在2007-2015年间的信用贷款情况数据,主要包括贷款状态和还款信息。附加属性包括:信用评分、地址、邮编、所在州等,累计75个属性(列),890000笔 贷款(行)。

- 贷款违约预测模型,使用了Numpy,Pandas,Sklearn科学计算包完成数据清洗,构建特征工程,以及完成预约模型的训练,数据可视化采用了Matplotlib及Seaborn等可视化包。

接下来,我们将利用给定的借贷数据,做一次较为完整的数据分析,进一步熟悉数据分析的流程。我们将分三个阶段来完成,分别是

-

数据的初步分析和整理

-

数据的探索性分析及可视化

-

借贷违约预测(LogisticRegression)

#导入相关库

import numpy as np

import pandas as pd

%matplotlib inline

import matplotlib.pyplot as plt

plt.style.use('ggplot') #风格设置近似R这种的ggplot库

import seaborn as sns

sns.set_style('whitegrid')

导入LendingClub贷款数据

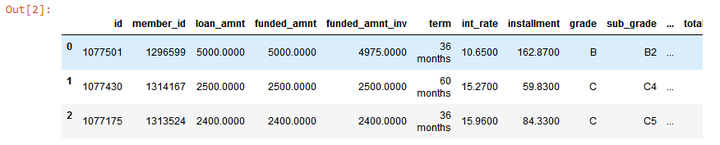

#导入数据及预览前三行

data=pd.read_csv("./dataset/loan.csv")

data.head(3)

本人电脑配置有限,为了加快计算速度,仅仅选择2015年度的贷款数据

#选择2015年度的贷款数据

data_15=data[(data.issue_d=='Jan-2015')\

|(data.issue_d=='Feb-2015')\

|(data.issue_d=='Mar-2015')\

|(data.issue_d=='Apr-2015')\

|(data.issue_d=='Apr-2015')\

|(data.issue_d=='Apr-2015')\

|(data.issue_d=='May-2015')\

|(data.issue_d=='Jun-2015')\

|(data.issue_d=='Jul-2015')\

|(data.issue_d=='Aug-2015')\

|(data.issue_d=='Sep-2015')\

|(data.issue_d=='Oct-2015')\

|(data.issue_d=='Nov-2015')\

|(data.issue_d=='Dec-2015')\

]

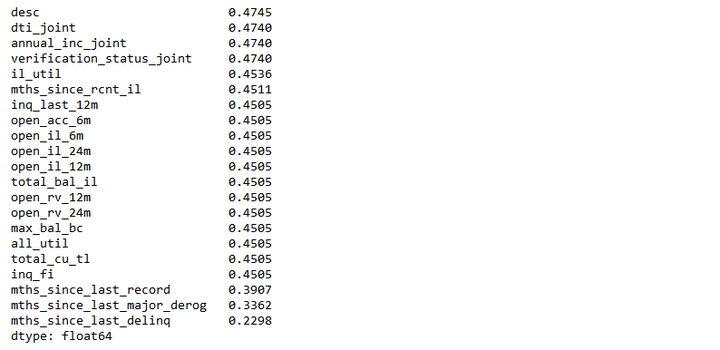

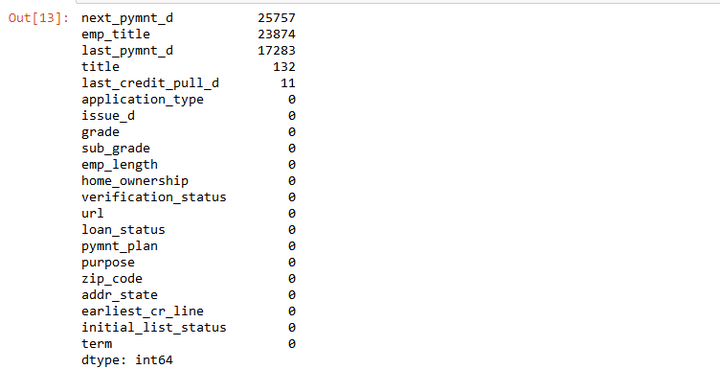

统计2015年度数据每列的缺失值情况。

#统计每列的缺失值情况

check_null = data_15.isnull().sum(axis=0).sort_values(ascending=False)/float(len(data)) #查看缺失值比例

print(check_null[check_null > 0.2]) # 查看缺失比例大于20%的属性。

从上图中可以看出,数据集中有很多列都有缺失值,所以我们要判断此列的数据对预测结果是否有影响,如果没有影响,可以将此列删除,本文中我们将缺失值超过40%的列删除。

#删除缺失值超过40%的列

thresh_count = len(data_15)*0.4 # 设定阀值

data_15 = data_15.dropna(thresh=thresh_count, axis=1 ) #若某一列数据缺失的数量超过阀值就会被删除

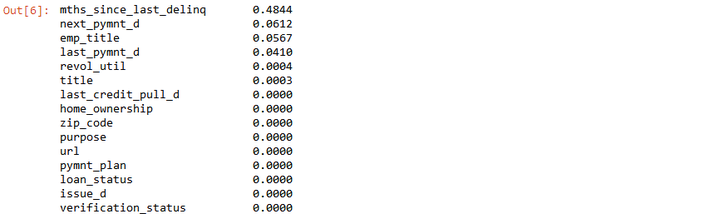

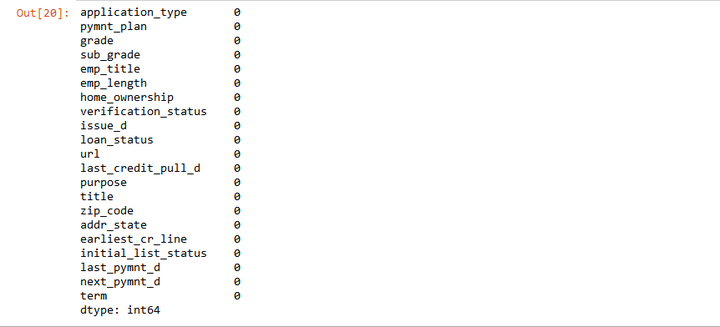

再次检查缺失值的情况,只有6列的数据还有缺失值。

#按缺失值比例从大到小排列

data_15.isnull().sum(axis=0).sort_values(ascending=False)/float(len(data_15))

查看数据类型的大概分布情况

data_15.dtypes.value_counts() # 分类统计数据类型

使用pandas的loc切片方法,得到每列至少有2个分类特征的数组集

#loc切片得到每列至少有2个分类特征的数组集

data_15 = data_15.loc[:,data_15.apply(pd.Series.nunique)!=1]

查看数据的变化,列数少了1列。

data_15.dtypes.value_counts()# 分类统计数据类型

上述过程,删除了较多缺失值的特征,以下将对有缺失值的特征进行处理

Object”和“float64“类型缺失值的处理方法不一样,所以将两者分开进行处理。

首先处理“Object”分类变量缺失值。

#便于理解将变量命设置为loans

loans=data_15

loans.shape

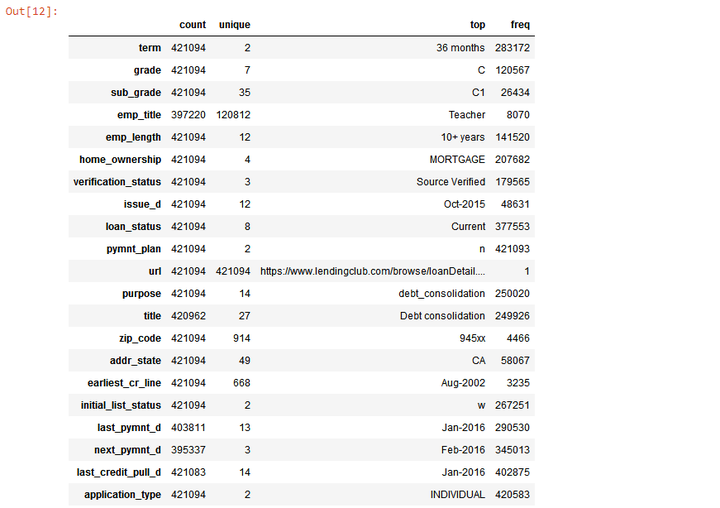

初步了解“Object”变量概况。

#初步了解“Object”变量概况

pd.set_option('display.max_rows',None)

loans.select_dtypes(include=['object']).describe().T

Object”分类变量缺失值概况。

#查看“Object”分类变量缺失值概况。

objectColumns = loans.select_dtypes(include=["object"]).columns

loans[objectColumns].isnull().sum().sort_values(ascending=False)

使用‘unknown’来填充缺失值。

#使用‘unknown’来填充缺失值

objectColumns = loans.select_dtypes(include=["object"]).columns # 筛选数据类型为object的数据

loans[objectColumns] = loans[objectColumns].fillna("Unknown") #以分类“Unknown”填充缺失值

确认“Object”分类变量无缺失值。

#查看“Object”分类变量缺失值情况

loans[objectColumns].isnull().sum().sort_values(ascending=False)

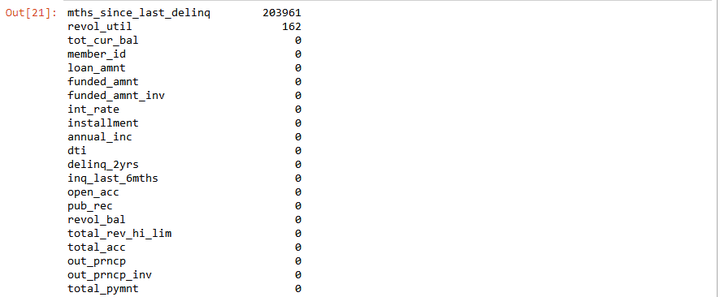

处理“float64”数值型变量缺失值。

loans.select_dtypes(include=[np.number]).isnull().sum().sort_values(ascending=False)

结果发现只有两个变量存在缺失值,使用mean值来填充缺失值。

#利用sklearn模块中的Imputer模块填充缺失值

numColumns = loans.select_dtypes(include=[np.number]).columns

from sklearn.preprocessing import Imputer

imr = Imputer(missing_values='NaN', strategy='mean', axis=0) # 针对axis=0 列来处理

imr = imr.fit(loans[numColumns])

loans[numColumns] = imr.transform(loans[numColumns])

再次查看数值变量缺失值。

loans.select_dtypes(include=[np.number]).isnull().sum().sort_values(ascending=False)

从上表中可以看到数值变量中已经没有缺失值。

本文的目的是对平台用户的贷款违约做出预测,所以需要筛选得到一些对用户违约有影响的信息,其他不相关的冗余信息,需要将其删除掉。

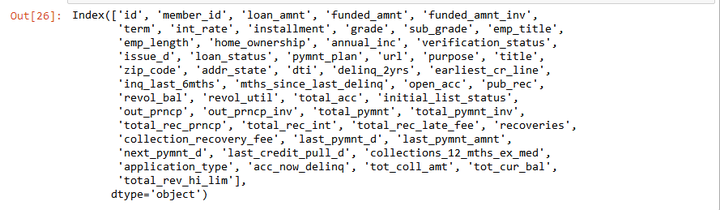

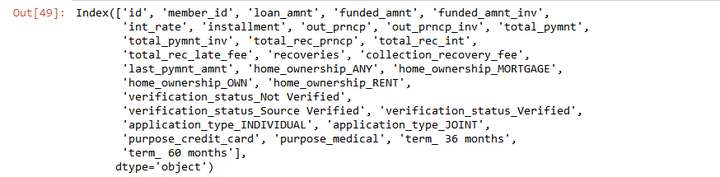

首先查看所有的分类标签

loans.columns

- sub_grade:与Grade的信息重复

- emp_title :缺失值较多,同时不能反映借款人收入或资产的真实情况

- zip_code:地址邮编,邮编显示不全,没有意义

- addr_state:申请地址所属州,不能反映借款人的偿债能力

- last_credit_pull_d :LendingClub平台最近一个提供贷款的时间,没有意义

- policy_code : 变量信息全为1

- pymnt_plan 基本是n

- title: title与purpose的信息重复,同时title的分类信息更加离散

- next_pymnt_d : 下一个付款时间,没有意义

- policy_code : 没有意义

- collection_recovery_fee: 全为0,没有意义

- earliest_cr_line : 记录的是借款人发生第一笔借款的时间

- issue_d : 贷款发行时间,这里提前向模型泄露了信息

- last_pymnt_d、collection_recovery_fee、last_pymnt_amnt: 预测贷款违约模型是贷款前的风险控制手段,这些贷后信息都会影响我们训练模型的效果,在此将这些信息删除

- url:所有的行都不同,没有分类意义

将以上重复或对构建预测模型没有意义的属性进行删除。

#删除对模型没有意义的列

loans2=loans.drop(['sub_grade', 'emp_title', 'title', 'zip_code', 'addr_state','url'], axis=1, inplace = True)

loans3=loans.drop(['issue_d', 'pymnt_plan', 'earliest_cr_line', 'initial_list_status', 'last_pymnt_d','next_pymnt_d','last_credit_pull_d'], axis=1, inplace = True)

再次查看‘Object’类型变量,只剩下8个分类变量。

object_columns_df3 =loans.select_dtypes(include=["object"]) #筛选数据类型为object的变量

print(object_columns_df3.iloc[0])

数据预处理完后,接下来探索数据的特征工程,为后续的违约预测模型做好建模准备工作

特征工程是机器学习最重要的一部分,希望找到的特征是最贴近实际业务场景的,所以要反复去找特征,只需要最少的特征得到简单的模型,并且有最好的预测效果。

本节将特征工程主要分3大部分:特征抽象 、特征缩放 、特征选择

数据集中有很多的“Object”类型的分类变量存在,但是对于这种变量,机器学习算法不能识别,需要将其转化为算法能识别的数据类型。

首先对于"loan_status"数据类型转换

#统计"loan_status"数据的分布

loans['loan_status'].value_counts()

将上表中的违约编码为1,正常的为0进行编码。

#使用Pandas replace函数定义新函数:

def coding(col, codeDict):

colCoded = pd.Series(col, copy=True)

for key, value in codeDict.items():

colCoded.replace(key, value, inplace=True)

return colCoded

#把贷款状态LoanStatus编码为违约=1, 正常=0:

pd.value_counts(loans["loan_status"])

loans["loan_status"] = coding(loans["loan_status"], {'Current':0,'Fully Paid':0\

,'In Grace Period':1\

,'Late (31-120 days)':1\

,'Late (16-30 days)':1\

,'Charged Off':1\

,"Issued":1\

,"Default":1\

,"Does not meet the credit policy. Status:Fully Paid":1\

,"Does not meet the credit policy. Status:Charged Off":1})

print( '\nAfter Coding:')

pd.value_counts(loans["loan_status"])

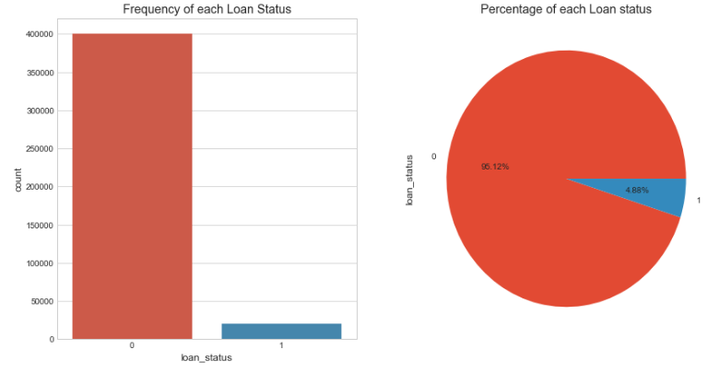

可视化查看"loan_status"中不同状态的替换情况。

# 贷款状态分布可视化

fig, axs = plt.subplots(1,2,figsize=(14,7))

sns.countplot(x='loan_status',data=loans,ax=axs[0])

axs[0].set_title("Frequency of each Loan Status")

loans['loan_status'].value_counts().plot(x=None,y=None, kind='pie', ax=axs[1],autopct='%1.2f%%')

axs[1].set_title("Percentage of each Loan status")

plt.show()

变量“emp_length”、"grade"进行特征抽象化

# 构建mapping,对有序变量"emp_length”、“grade”进行转换

mapping_dict = {

"emp_length": {

"10+ years": 10,

"9 years": 9,

"8 years": 8,

"7 years": 7,

"6 years": 6,

"5 years": 5,

"4 years": 4,

"3 years": 3,

"2 years": 2,

"1 year": 1,

"< 1 year": 0,

"n/a": 0

},

"grade":{

"A": 1,

"B": 2,

"C": 3,

"D": 4,

"E": 5,

"F": 6,

"G": 7

}

}

loans = loans.replace(mapping_dict) #变量映射

loans[['emp_length','grade']].head() #查看效果

变量"home_ownership", "verification_status", "application_type","purpose", "term" 狂热编码

#变量狂热编码

n_columns = ["home_ownership", "verification_status", "application_type","purpose", "term"]

dummy_df = pd.get_dummies(loans[n_columns])# 用get_dummies进行one hot编码

loans = pd.concat([loans, dummy_df], axis=1) #当axis = 1的时候,concat就是行对齐,然后将不同列名称的两张表合并

loans = loans.drop(n_columns, axis=1) #清除原来的分类变量

重新查看数据集中的数据类型

loans.info() #查看数据信息

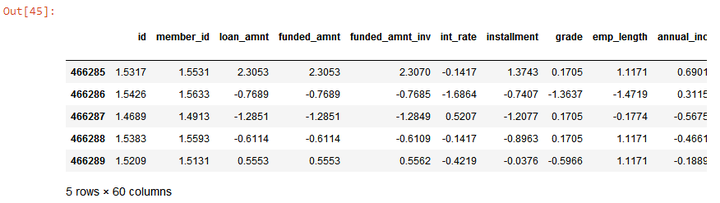

采用标准化的方法进行去量纲操作,加快算法收敛速度,采用scikit-learn模块preprocessing的子模块StandardScaler进行操作。

col = loans.select_dtypes(include=['int64','float64']).columns

col = col.drop('loan_status') #剔除目标变量

loans_ml_df = loans # 复制数据至变量loans_ml_df

from sklearn.preprocessing import StandardScaler # 导入模块

sc =StandardScaler() # 初始化缩放器

loans_ml_df[col] =sc.fit_transform(loans_ml_df[col]) #对数据进行标准化

loans_ml_df.head() #查看经标准化后的数据

以上过程完成了非数值型特征抽象化处理,使得算法能理解数据集中的数据,这么多的特征,究竟哪些特征对预测结果影响较大,所以以下通过影响大小对特征进行选择。

特征的选择优先选取与预测目标相关性较高的特征,不相关特征可能会降低分类的准确率,因此为了增强模型的泛化能力,我们需要从原有特征集合中挑选出最佳的部分特征,并且降低学习的难度,能够简化分类器的计算,同时帮助了解分类问题的因果关系。

一般来说,根据特征选择的思路将特征选择分为3种方法:嵌入方法(embedded approach)、过滤方法(filter approach)、包装方法(wrapper approacch)。

- 过滤方法(filter approach): 通过自变量之间或自变量与目标变量之间的关联关系选择特征。

- 嵌入方法(embedded approach): 通过学习器自身自动选择特征。

- 包装方法(wrapper approacch): 通过目标函数(AUC/MSE)来决定是否加入一个变量。

本次项目采用Filter、Embedded和Wrapper三种方法组合进行特征选择。

首先将数据集中的贷款状态'loan_status'抽离出来

#构建X特征变量和Y目标变量

x_feature = list(loans_ml_df.columns)

x_feature.remove('loan_status')

x_val = loans_ml_df[x_feature]

y_val = loans_ml_df['loan_status']

len(x_feature) # 查看初始特征集合的数量

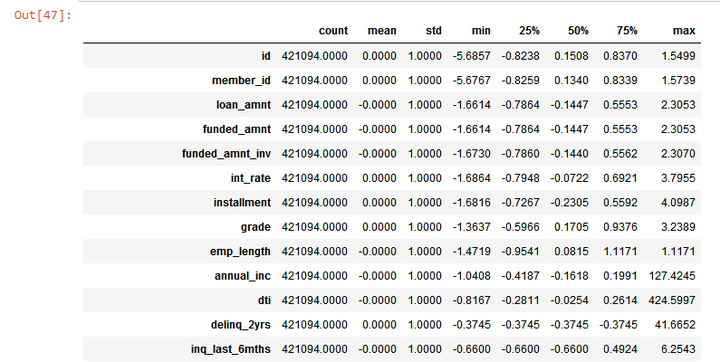

重新查看没有贷款状态'loan_status'的数据集。

x_val.describe().T # 初览数据

Wrapper方法

选出与目标变量相关性较高的特征。通过暴力的递归特征消除 (Recursive Feature Elimination)方法筛选30个与目标变量相关性最强的特征,将特征维度从59个降到30个。

from sklearn.feature_selection import RFE

from sklearn.linear_model import LogisticRegression

# 建立逻辑回归分类器

model = LogisticRegression()

# 建立递归特征消除筛选器

rfe = RFE(model, 30) #通过递归选择特征,选择30个特征

rfe = rfe.fit(x_val, y_val)

# 打印筛选结果

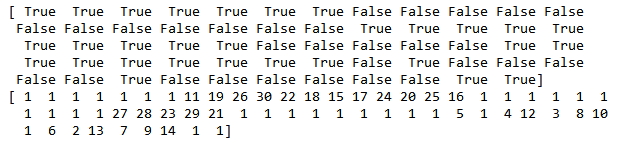

print(rfe.support_)

print(rfe.ranking_) #ranking 为 1代表被选中,其他则未被代表未被选中

通过布尔值筛选首次降维后的变量。

col_filter = x_val.columns[rfe.support_] #通过布尔值筛选首次降维后的变量

col_filter # 查看通过递归特征消除法筛选的变量

Filter方法

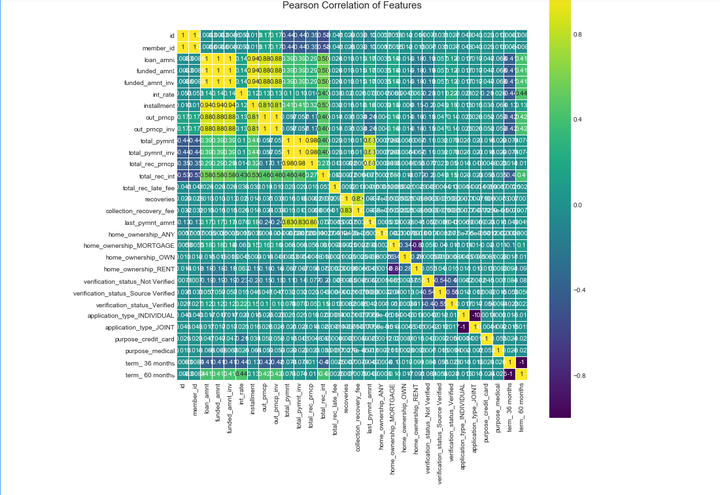

正常情况下,影响目标变量的因数是多元性的;但不同因数之间会互相影响(共线性 ),或相重叠,进而影响到统计结果的真实性。下一步,以下通过皮尔森相关性图谱找出冗余特征并将其剔除,且通过相关性图谱进一步引导我们选择特征的方向。

colormap = plt.cm.viridis

plt.figure(figsize=(12,12))

plt.title('Pearson Correlation of Features', y=1.05, size=15)

sns.heatmap(loans_ml_df[col_filter].corr(),linewidths=0.1,vmax=1.0, square=True, cmap=colormap, linecolor='white', annot=True)

从上图中得到需要删除的冗余特征。

drop_col = ['id','member_id','collection_recovery_fee','funded_amnt', 'funded_amnt_inv','installment', 'out_prncp', 'out_prncp_inv',

'total_pymnt_inv', 'total_rec_prncp', 'total_rec_int', 'home_ownership_OWN',

'application_type_JOINT', 'home_ownership_RENT' ,

'term_ 36 months', 'total_pymnt', 'verification_status_Source Verified', 'purpose_credit_card','int_rate']

col_new = col_filter.drop(drop_col) #剔除冗余特征

print(len(col_new))

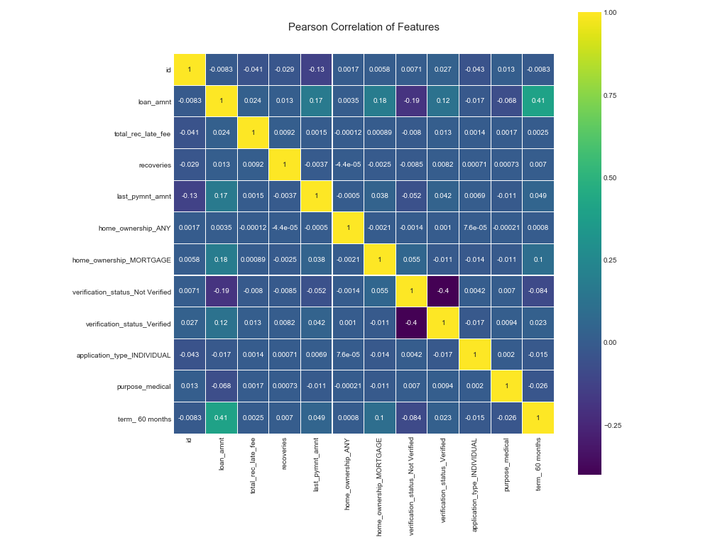

特征从30个降到12个,再次确认处理后的数据相关性。

col_new # 查看剩余的特征

colormap = plt.cm.viridis

plt.figure(figsize=(12,12))

plt.title('Pearson Correlation of Features', y=1.05, size=15)

sns.heatmap(loans_ml_df[col_new].corr(),linewidths=0.1,vmax=1.0, square=True, cmap=colormap, linecolor='white', annot=True)

Embedded方法

为了了解每个特征对贷款违约预测的影响程度,所以在进行模型训练之前,我们需要对特征的权重有一个正确的评判和排序,就可以通过特征重要性排序来挖掘哪些变量是比较重要的,降低学习难度,最终达到优化模型计算的目的

#随机森林算法判定特征的重要性

names = loans_ml_df[col_new].columns

from sklearn.ensemble import RandomForestClassifier

clf=RandomForestClassifier(n_estimators=10,random_state=123)#构建分类随机森林分类器

clf.fit(x_val[col_new], y_val) #对自变量和因变量进行拟合

names, clf.feature_importances_

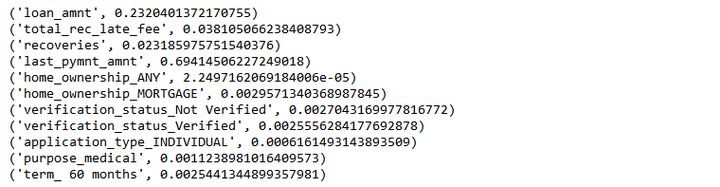

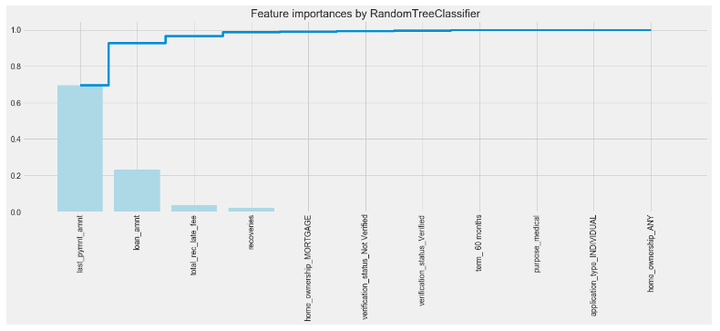

for feature in zip(names, clf.feature_importances_):

print(feature)

特征重要性从大到小排序及可视化图形,结果发现最具判别效果的特征是收到的最后付款总额‘last_pymnt_amnt’

本项目中,2015年度贷款平台上违约的借款人比例很低,约为4.9%,正负样本量非常不平衡,非平衡样本常用的解决方式有2种:

-

过采样(oversampling),增加正样本使得正、负样本数目接近,然后再进行学习。

-

欠采样(undersampling),去除一些负样本使得正、负样本数目接近,然后再进行学习。

#构建自变量和因变量

X = loans_ml_df[col_new]

y = loans_ml_df["loan_status"]

n_sample = y.shape[0]

n_pos_sample = y[y == 0].shape[0]

n_neg_sample = y[y == 1].shape[0]

print('样本个数:{}; 正样本占{:.2%}; 负样本占{:.2%}'.format(n_sample,

n_pos_sample / n_sample,

n_neg_sample / n_sample))

print('特征维数:', X.shape[1])

from imblearn.over_sampling import SMOTE # 导入SMOTE算法模块

# 处理不平衡数据

sm = SMOTE(random_state=42) # 处理过采样的方法

X, y = sm.fit_sample(X, y)

print('通过SMOTE方法平衡正负样本后')

n_sample = y.shape[0]

n_pos_sample = y[y == 0].shape[0]

n_neg_sample = y[y == 1].shape[0]

print('样本个数:{}; 正样本占{:.2%}; 负样本占{:.2%}'.format(n_sample,

n_pos_sample / n_sample,

n_neg_sample / n_sample))

采用逻辑回归分类器 分类器进行训练

# 构建逻辑回归分类器

from sklearn.linear_model import LogisticRegression

clf1 = LogisticRegression()

clf1.fit(X, y)

查看预测结果的准确率

predicted1 = clf.predict(X) # 通过分类器产生预测结果

from sklearn.metrics import accuracy_score

print("Test set accuracy score: {:.5f}".format(accuracy_score(predicted1, y,)))

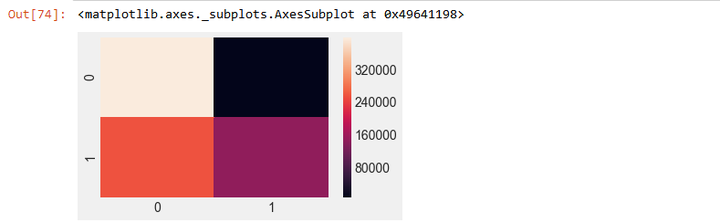

利用混淆矩阵及可视化观察预测结果

#生成混淆矩阵

from sklearn.metrics import confusion_matrix

confusion_matrix(y, predicted1)

# 混淆矩阵可视化

plt.figure(figsize=(5,3))

sns.heatmap(m)

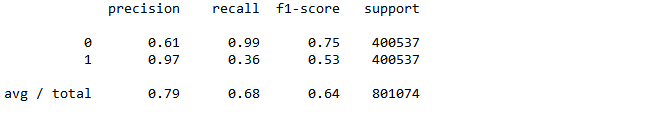

再利用sklearn.metrics子模块classification_report查看precision、recall、f1-score的值

#查看precision、recall、f1-score的值

from sklearn.metrics import classification_report

print(classification_report(y, predicted1))

#计算ROC值

from sklearn.metrics import roc_auc_score

roc_auc1 = roc_auc_score(y, predicted1)

print("Area under the ROC curve : %f" % roc_auc1)

以上完成了全部的模型训练及预测工作。

本文基于互联网金融平台2015年度贷款数据完成信贷违约预测模型,全文包括了数据清洗,构建特征工程,训练模型,最后得到的模型准确率达到了0.79,召回率达到了0.68,具有较好的预测性,本文的模型可以作为信贷平台预测违约借款人的参考